New: Get your FICO® scores inside Dispute Beast – the same scores 90% of lenders use!

Rated 4.8 Stars by over 2,888 Users

The most advanced AI Financial app ever created

Your ultimate DIY credit repair dispute assistant tool powered by AI with a 110% Money-back guarantee.

Get Started

Making your dispute letters with Dispute Beast's engine is free. But, you need Beast Credit Monitoring to do it. It's $49.99 a month. If you have Beast Credit Monitoring, you can make as many letters as you want in Dispute Beast.

Your AI-Powered Credit Assistant

Millions endure a struggle due to poor credit scores, you can avoid that

Join 100,000+ users who've improved their credit with our DIY credit repair tools. Dispute errors, track progress, and reach your dream score faster.

"What? Why did my credit score go down?"

"I am just not able to get rid of this interest on my card!"

"Why can't I get an increase on my credit limit?"

"It's been months and I just can't get approved for my new home."

"I just can't catch a break with all of this interest piling up on me."

"Where did all these negative accounts come from?"

Full control of your Credit

Equipping you with the ability to take full control of your Financial health

At Dispute Beast, we aim to be more than just another credit app. We strive to become your trusted partner in your pocket, dedicated to helping you on your financial journey.

AI that helps you take control of your Credit financial future

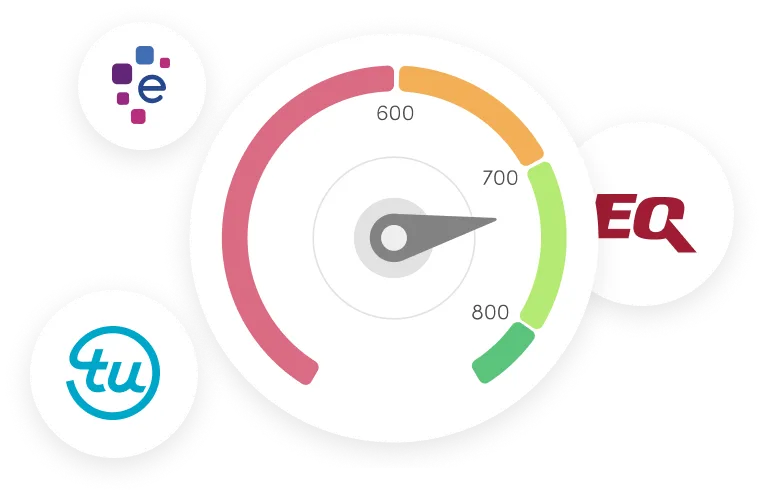

Financial overview &

Scores from all 3 Bureaus

Cost should never be a barrier when it comes to improving personal financial health, and we stand by this.

AI Disputing Engine that

does the hard

work for you

Our AI engine reviews and highlights the negative items in your report, you'll know what to attack.

How It Works

How Dispute Beast's AI Removes Negative items

Traditional credit repair companies charge $250/month or more for basic dispute letters. Our AI credit repair software revolutionizes the process, it just takes a few minutes to get started:

AI Credit Analysis

Our software scans your credit report for errors and negative items

Smart Dispute Letters

AI generates legally-compliant dispute letters personalized to your situation

Automated Mailing

Letters sent via USPS through our mailing partner Sprint Mail. Track your order's progress online.

Progress Tracking

Monitor results across all 3 Bureaus and review notable changes easily with our tools.

Get the power of AI for your Credit in your pocket for as low as $49.99/m.

3-Bureau Credit monitoring required to use Dispute Beast’s AI features. Both VantageScore® and FICO® scores available.

4.8 Stars · 2,888 Reviews

Trustpilot 4.4/5 · 1,562 Reviews

Your Real FICO® 8 Scores, Inside Beast

- FICO® 8 from all 3 bureaus — the scores 90% of lenders use

- Daily monitoring with zero credit impact

- AI disputes prioritized by FICO® score impact

How it Works

Advanced AI Credit

Repair Features

From dispute letters to progress tracking, AI handles the hard work so you don't have to.

AI Dispute Letter Generator

No templates. Our AI analyzes your credit profile and generates personalized, legally-compliant letters that bureaus & creditors actually respond to.

Mail 10+ Letters in just a click

Our AI automatically identifies questionable items across all bureaus and launches targeted attacks simultaneously with one click.

Automatic Negative Account Filtering

Not all negative items are worth disputing. Our AI ranks every mark by removal probability and score impact, focusing on disputes that will move your score the most.

Your New Credit Report Progress Tracker

Watch your score climb in real-time. Track every dispute, monitor bureau responses, and see exactly how each removal impacts your credit score across all three bureaus.

Money-Back Guarantee like no other

We guarantee score improvement or you get every penny back. Our system automatically handles all bureau responses—no manual follow-up required.

Trusted by thousands of users

“An absolute game-changer when it comes to resolving disputes.”

Ron L.“After the 1st round, my score shot up over 220 points.”

John M.“I recommend this service to all my friends and family. It really works!”

Remy A.“The platform's user-friendly interface made it incredibly easy for me”

Irvin J. "Extremely easy to use"

Start your DIY process in just 5 minutes

When you’re enrolled with Beast Monitoring partner service, using Dispute Beast is entirely free to dispute letters. We’re offering an entirely new & automated AI credit disputing solution to improve your scores.

Step 1

Sign up for Monitoring & get your Free Dispute Beast account

All you need is active Beast Monitoring, the rest is on us. Monitoring is a monthly subscription that costs $49.99, and provides you with advanced 3-Bureau reports on your credit so you can have a better idea of your financial status.

Step 2

Get your full Credit Report & get clarity on what is affecting you

Get access to your full credit report from all 3 Bureaus, understand in full detail what is hurting and affecting your credit score. It’s time to address what has been stopping you from reaching your goals.

Step 3

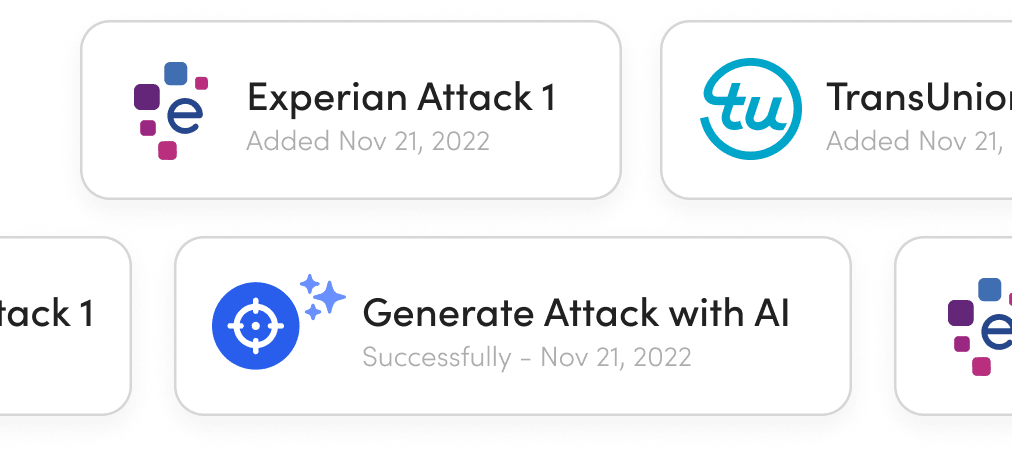

Attack using our AI disputing engine, it'll do it all for you!

Our proprietary BeastAI engine has processed close to a million letters to dispute erroneous items on consumer’s accounts. Take a full in-depth view into your credit report using our smart filter, and start your first Attack to get rid of any erroneous items on your report.

Step 4

Mail Attack

You've created your attack. Now it's time to mail it out. Choose your path:

- Sprint Mail (Paid) – One click. Everything handled for you: printing, packaging, mailing — even tracking. Sent via 1st Class without the hassle. Fast, reliable, and no trips to the post office.

- Free Download (DIY) – Want full control? Download your letters, print at home (don't forget ink and envelopes), stuff, stamp, and head to the post office. Free, but manual.

This step matters. The faster your letters go out, the faster credit bureaus must respond. Each Attack moves you closer to better scores. Stay consistent, be patient, repeat the process.

We've helped thousands of users increase their credit score

Get Started

Dispute Beast 110% Money-Back Guarantee

We believe in the quality of our products. If you’re not satisfied, we will return 110% (yes, 110!) back of your money if Dispute Beast doesn’t help you improve your credit after a year.

Secure & Reliable

Our platform holds the highest standards of security, and our customer support team is available 24/7 to assist you throughout the process.

Risk-Free Process

Built to deliver real results. If no changes occur, every payment you’ve made will be fully refunded.

Trust & Transparency

We stand by the effectiveness of our service, which is why we offer the best guarantee in the credit repair industry.

Get Lender-Used FICO® Scores now inside of Dispute Beast

Access the same FICO® 8 scores that 90% of lenders use for credit decisions. Monitor your real credit health while Dispute Beast’s AI works to improve what matters most. Get started and choose between Vantage or FICO® today.

Credit Step-By-Step Guides